Markets have never moved on anything but information. However, in a world where thousands of financial news reports, earnings releases, and regulatory filings are published each hour, it is not the availability of information that is the problem, rather how to process it quickly enough to act on it. That is precisely where a news sentiment API comes into play.

Sentiment data derived through financial news is rapidly becoming a signal, not an add-on, whether you are a systematic trader running an algorithm, a quant constructing a multi-factor model, or a portfolio manager attempting to be ahead of macro moves.

What is a News Sentiment API?

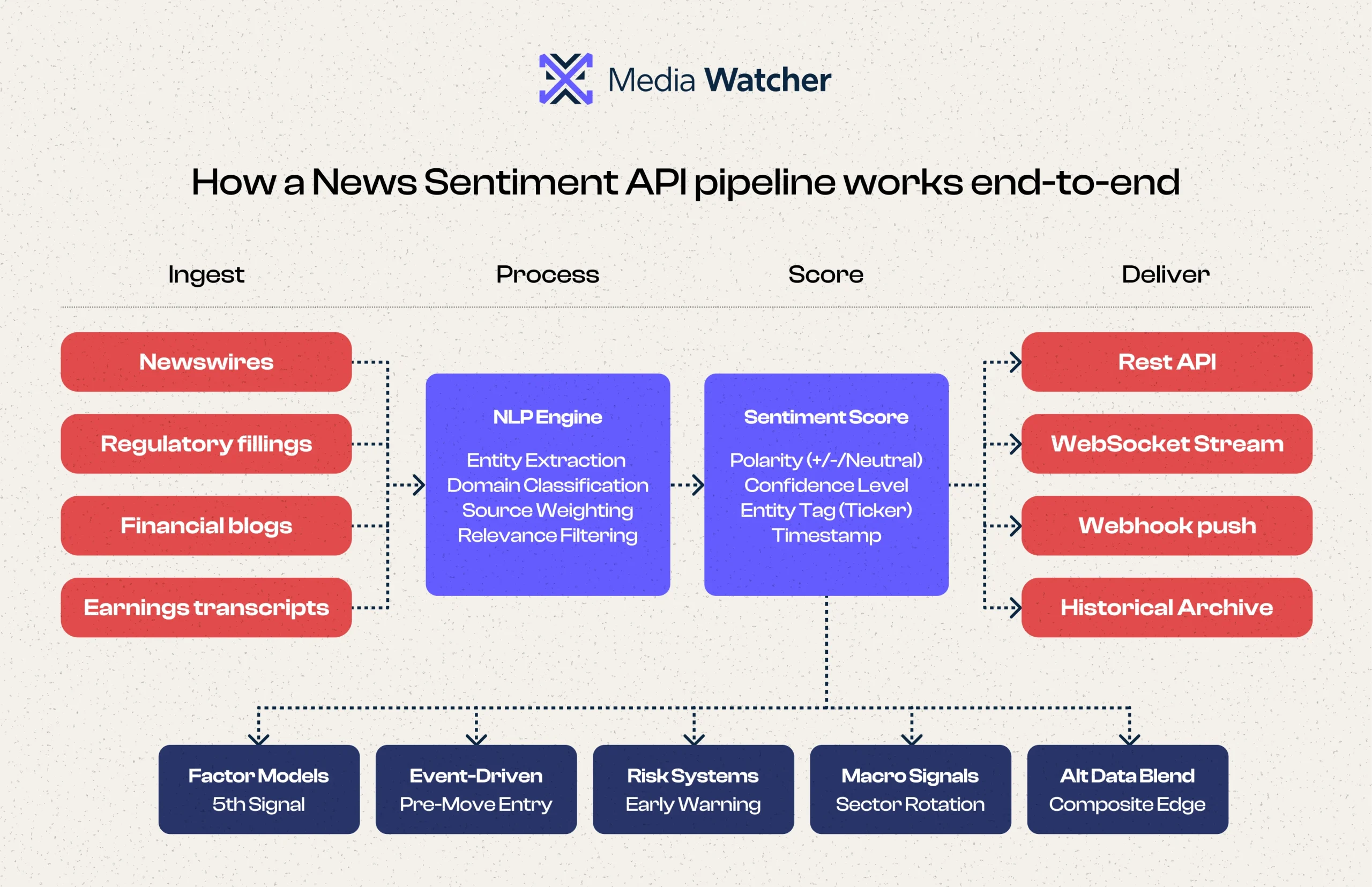

A news sentiment API is a programmable interface that accepts news content across financial media, applies Natural Language Processing (NLP) and machine learning models to it, and returns structured sentiment scores, often positive, negative, or neutral, and metadata such as source, relevance, entity tags, and timestamp.

Think of it as a layer of intelligence sitting between raw news and your trading system. In place of manually processing thousands of headlines, the API will do so automatically and at scale, sending machine-readable sentiment signals straight into your models, dashboards, or execution engines.

An effective financial news sentiment API does not simply declare a headline as positive or negative. It tells what asset, company, or sector the sentiment is regarding, the confidence of the model, how material the source is, and how the sentiment is relative to recent historical baselines of that entity.

Why Sentiment Data Has Become a Core Trading Signal

Price is a lagging indicator. By the time a price move is visible on a chart, the smart money has already reacted. Instead, news sentiment is a leading or coincidental indicator that trades market-moving information at the time it becomes known.

Decades of academic research demonstrate that media tone is predictive of short-term stock returns. This has been supported by more recent research with large-scale NLP models, which demonstrates that stock sentiment API data systematically enhances stock returns in both long-short equity strategies and volatility forecasting.

There are several concrete reasons why sentiment has become a reliable edge:

Processing speed: Thousands of articles cannot be read and scored by human analysts in real-time. A trading sentiment API can process an earnings release, a central bank statement, and a geopolitical news story simultaneously and route the appropriate signal to the right strategy within milliseconds.

Minimization of emotional bias: Discretionary traders are vulnerable to anchoring and recency bias. The subjectivity of algorithms is eliminated through algorithmic sentiment signals, which use the same scoring criteria for all events.

Breadth of coverage: A sophisticated financial media monitoring API consolidates financial blogs, newswires, regulatory documents, and specialized publications, which provides the quants with the complete picture, not just a fragmented one.

How Quants and Traders Actually Use It

A stock market sentiment API has practical uses across the entire range of trading strategies.

1. Event-Driven Trading

Concentrated bursts of news are produced by announcements of earnings, central bank decisions, and corporate actions. Sentiment APIs have the ability to identify the tone of an earnings call transcript in real-time, before it has been fully digested by the larger market. Quants take this to take a position before or right after the sentiment change.

2. Factor Model Enhancement

Multi-factor models, which are value, momentum, quality, and growth signals, are commonly constructed by quantitative portfolio managers. Sentiment is also becoming a fifth factor, in addition to or as a filter to prevent getting into positions with strongly negative news sentiment, despite the attractiveness of other factors.

3. Prevention of Risk and Drawdown

An early warning system can be a news monitoring API. When the market sentiment around a core holding is becoming very negative, and the price is not yet moving, a risk system can proactively decrease the exposure. This can be particularly useful when dealing with tail risk in geopolitical events or shocks in the sector.

4. Macro and Thematic Signals

In addition to single stocks, quants rely on aggregate sector, currency, or commodity-wide sentiment to create macro views. An increasing wave of adverse attitude in the news of the energy sector, such as, can be an indication of a sector rotation opportunity that needs to be confirmed by price data.

5. Alternative Data Strategies

Institutional investors are moving toward incorporating news sentiment with other alternative data streams, including satellite imagery, credit card transaction data, and web traffic, to create more informational advantages. The connective tissue of these composite models is the financial news sentiment API.

What to Look For in a News Sentiment API

Not all sentiment APIs are equal. The quality of the underlying NLP model, the breadth of source coverage, the latency of delivery, and the granularity of entity tagging all vary significantly. Here’s what separates a professional-grade API from a generic one:

- Financial domain training: General-purpose sentiment models trained on social media or product reviews often misclassify financial language. Look for models specifically trained on financial corpora.

- Entity-level scoring: You need sentiment attributed to a specific ticker or company, not just the article as a whole.

- Source quality weighting: Not all news sources carry equal market weight. A well-designed API weights signals by source credibility and relevance.

- Historical data access: Backtesting requires clean historical sentiment data going back years. Without it, you can’t validate your strategy.

- Low-latency delivery: For intraday strategies, delivery lag matters. Real-time streaming via WebSocket or webhook is preferable to polling-based REST APIs.

Ready to Scale Your Financial Intelligence with Media Watcher?

Media Watcher is a professional-grade financial media monitoring API and news intelligence platform purpose-built for traders, quants, and investment professionals who need structured, high-quality sentiment data flowing into their systems.

Media Watcher goes beyond surface-level sentiment scoring. It delivers entity-tagged, source-weighted, financially-tuned sentiment signals across a comprehensive universe of global financial news in real time. Whether you’re plugging it into a Python-based quant model, a Bloomberg terminal workflow, or a custom trading dashboard, Media Watcher’s API is designed for seamless integration with minimal engineering overhead.

The platform also provides historical sentiment archives, enabling rigorous backtesting and factor validation. Its news monitoring API layer continuously ingests from thousands of sources, newswires, regulatory filings, financial news platforms, and earnings transcripts, so no market-moving story slips through.

For teams that take information edge seriously, Media Watcher isn’t just a data vendor. It’s infrastructure.

Ready to integrate real-time news sentiment into your trading workflow? Explore what Media Watcher can do for your strategy.