On April 2, 2025, President Trump announced new taxes on imported goods called tariffs, meaning foreign countries would be charged more to sell their products in the US. The Standard’s and Poor’s (S&P) 500 shed 11% over the following two trading sessions.

Whereupon the Federal Reserve Bank of San Francisco described this as one of the sharpest declines in decades. The energy sector fell 17% in those same two days.

Supplementary sentiment research on that event confirmed that negative media tone and market downturns moved closely together, with narrative framing amplifying investor uncertainty well before the full price response was visible in data.

An equity analyst relying on price feeds during those 36 hours saw the S&P move. A developer whose pipeline consumed a financial news API with real-time sentiment scoring saw the narrative building in regional trade and financial media before the price confirmed it.

Thus, the gap between when a narrative forms and when price reflects it is what the blog covers.

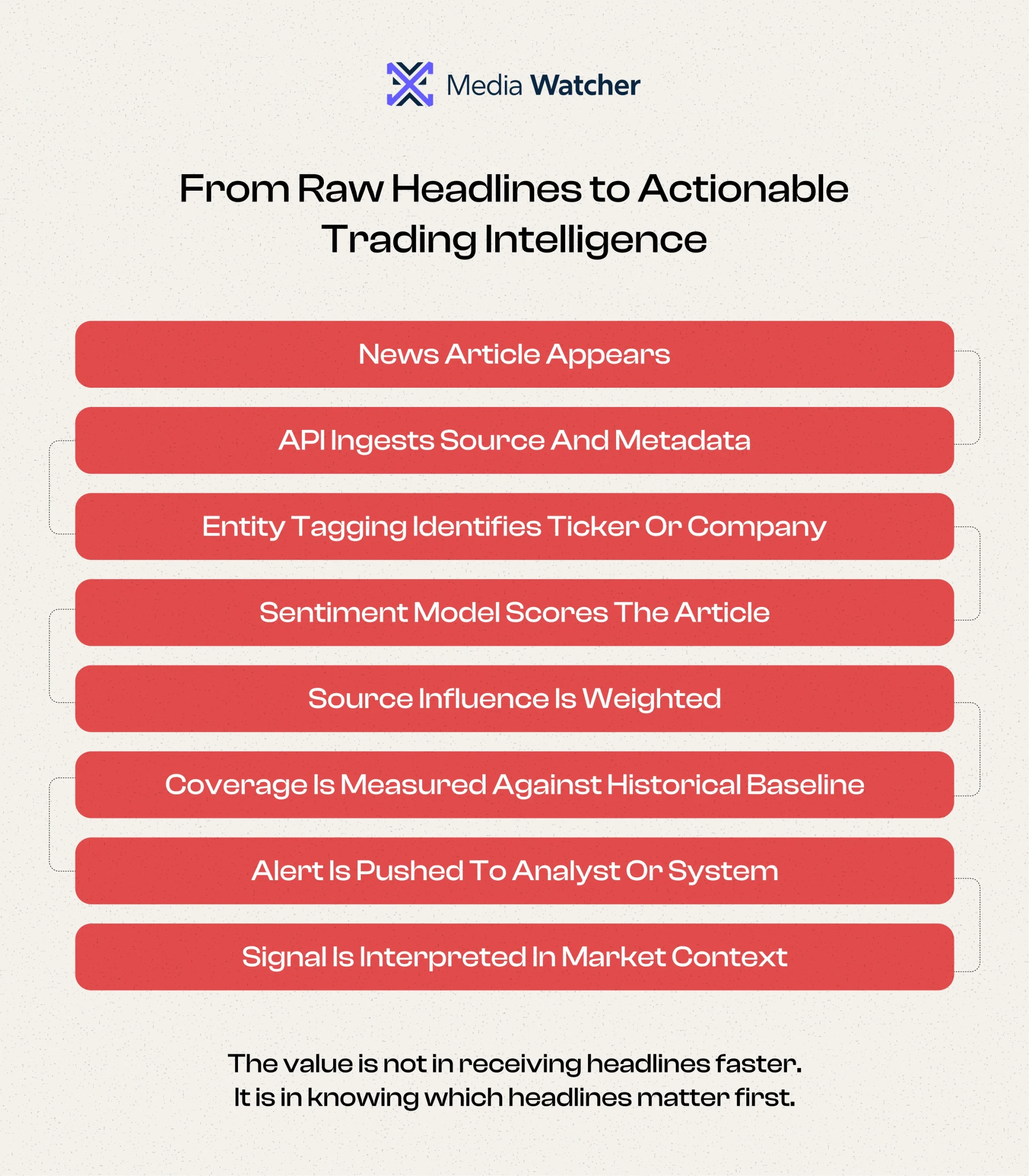

What a Financial News API Actually Delivers

The financial news API is a programming interface that provides developers with access to financial information on news articles, sentiment, and metadata for financial instruments.

Instead of using web scraping or having manual data feeds, the developer sends requests to the API by providing a ticker or keywords in order to get relevant information.

The core data types a financial news API exposes are: article metadata, entity tagging, sentiment scores per article, coverage volume signals relative to a ticker’s historical baseline, and source attribution.

The quality of each layer varies considerably across providers, and that variance is where signal quality diverges in production environments.

The financial data API will already be the dominant point of engagement for developers and end-users by 2026. Also, agentic processes have been incorporated into stock analysis, portfolio management, and risk control.

For a prop trader or equity analyst evaluating real-time financial data API options, the relevant question is not documentation quality or pricing tier. It is whether the sentiment methodology and source coverage are deep enough to produce actionable signals before the price reacts.

Why Price Data Alone Creates a Timing Problem

Price data confirms what market participants have already done. Narrative is what they are currently processing. The gap between those two states is where early-mover positioning either exists or does not.

This is not a new observation. Tetlock’s 2007 study in the Journal of Finance, analyzing daily content from a Wall Street Journal column, established that high media pessimism predicts downward pressure on market prices ahead of the move, and that unusually high or low pessimism predicts elevated trading volume.

Baker and Wurgler’s foundational 2006 paper in the same journal established that investor sentiment, as measured by market proxies, predicts subsequent cross-sectional stock returns.

What has changed is the infrastructure available to act on it. A financial news API that delivers articles without sentiment scoring, without source authority weighting, and without historical baseline comparison is an information pipe.

A well-configured market news API that includes all three layers is an intelligence infrastructure. The challenge for developers in 2026 is not accessing financial news.

It is distinguishing between those two categories of tools before building on the wrong one.

Three Challenges Developers Face When Building on Financial News APIs

Listed below are the three core challenges faced by developers when they are building financial news APIs

NLP Model Selection Determines Signal Quality.

Financial news APIs return a sentiment score. Few document which model produced it. General-purpose sentiment models were designed for social media and customer review text.

They encounter consistent difficulty with the specialized language of earnings releases, regulatory filings, and macroeconomic commentary. Finance-specific models are trained on financial text and handle these language patterns substantially better.

Developers who treat sentiment scoring as a commodity and accept the default model selection produce lower signal quality in production.

Source Breadth Determines How Early The Signal Arrives.

A stock news API drawing from a few hundred sources misses the tier-2 financial outlets, regional trade publications, and sector-specific media where stories often appear before major wire services carry them.

The April 2025 tariff event had approximately 36 hours of narrative build in regional financial and trade media before the full institutional repricing occurred, according to FRBSF analysis. A pipeline monitoring only major English-language sources would have seen the story far later in that sequence.

The signal arrives early from the edges of the media landscape, not from its center.

Equal-Count Scoring Obscures Rather Than Surfaces Signals.

A financial data API news endpoint that counts article mentions equally treats a Reuters lead story identically to the same story syndicated across 40 aggregators. The Reuters article carries a different influence on market participant behavior.

Without source authority weighting, a developer’s system responds to noise as readily as it responds to signal. This is not a data quality problem in the traditional sense. The data is accurate. The scoring methodology is flawed.

What the Right Financial News API Infrastructure Looks Like

Developers building trading intelligence on financial news APIs need to evaluate against a specific set of criteria. The table below summarizes what matters and why.

| Criterion | What to Look For |

| Source breadth | Tens of thousands of sources minimum, covering regional and trade publications in addition to wire services. Language and region coverage matter as much as total source count. |

| NLP methodology | Finance-specific model. Ask the vendor which model is used and which training data it was trained on. General-purpose models produce materially weaker results on financial language. |

| Source authority weighting | The system should weight articles by source influence, not treat all mentions equally. This separates the signal from amplified noise. |

| Alert latency | Sub-200 ms from the source publication for trading-grade pipelines. Any longer and the signal may arrive after institutional desks have already acted. |

| Delivery format | HTTP Post or WebSocket for event-driven pipelines. REST polling introduces unnecessary latency for live trading applications. |

| Historical depth | Multi-year archives with consistent NLP scoring methodology for backtesting sentiment-driven strategies. |

How Investment Watcher Addresses These Challenges

Investment Watcher is the media intelligence layer that sits on top of price and fundamental data. It is built on Media Watcher’s infrastructure, which monitors 100,000+ media sources in real time across 80+ languages and 235+ regions, with media alerts delivered within 200ms of source publication via email, Slack, iOS, Android, or HTTP Post.

The Influence Score addresses the source authority problem directly. Rather than counting article mentions equally, it weights news sources by their demonstrated influence on market participant behavior.

A story breaking in a tier-1 financial outlet carries a different signal weight than the same story syndicated across aggregators 90 minutes later.

This distinction separates genuine narrative formation from noise amplification.

HTTP Post alert delivery addresses the latency and pipeline integration problem. Real-time narrative signals feed directly into event-driven trading systems without polling overhead, keeping delivery within the sub-200ms infrastructure window.

The Market Sentiment Context Line addresses the cross-signal interpretation problem.

It runs alongside portfolio-level news monitoring, surfacing divergences between market-wide fear and greed readings and the sentiment building around specific holdings.

A developer consuming Investment Watcher’s narrative signals saw the story building in regional media before that confirmation arrived.

This is the difference between a financial news API used as a data pipe and a media intelligence API used as a trading intelligence layer.

Most developers integrating a financial news API are solving the data access problem. They are not yet solving the narrative interpretation problem: which sources carry weight, when sentiment is shifting before price confirms it, and how a specific ticker’s media story compares to the broader market mood at the same moment.

The window between narrative formation and price confirmation is consistent and measurable. Developers who need to see it first need infrastructure designed for that task.

Standard financial news APIs deliver data. Investment Watcher delivers the narrative layer that precedes it.

Book a Demo at Media Watcher to see how the media intelligence API layer closes the gap your current stock news API leaves open.